Offer Financing to Customers to Improve Close Rates

Why You Should Offer Financing to Customers

Appliances financing has long been an option for customers making large purchases (and it’s increasingly popular for small purchases too!) – and for good reason. When you have a wider net, you can catch more fish.

Enabling your customers to pay via externally financed loans ultimately gives you the ability to sell to more people. Some prospects will need your services, but simply can’t afford to pay for significant work all at once. Make sure you don’t turn these willing customers away. Further, offering financing makes it easier to win bigger jobs!

There are many reasons that a customer may choose to pay via financing; we all know that big purchases can be daunting. Appliance financing downsizes an enormous financial commitment into manageable segments and limits the risk of you not getting paid. And as a bonus, when payments are split into smaller portions, you may notice that customers are willing to spend more overall too.

Of course, many trades businesses are already offering financing to customers. Many also offer flexible payment options – and perhaps your business does too. But answer this question: is financing appliances currently a burden in your sales process?

Financing should help you close more deals and sell to more people, but instead many businesses find that the paperwork and admin required to get appliances financing approved can sometimes kill the sale itself. Especially if your workforce is stretched thin. But it doesn’t have to be that way.

Common Challenges Associated with Offering Financing in the Trades

Legal and Regulatory Compliance: Offering in-house financing is rare for smaller service businesses. After all, running credit checks, overseeing legal risks, and is time-consuming and delicate without the right support. That’s why most trades businesses who offer financing work with a financing partner.

Interest Rates and Terms: Working with a financial provider comes with service, late, and early repayment fees. It’s crucial to explore and understand what different partners offer, and how it impacts your customers. Additionally, fees associated with your financial partner will affect the acquisition cost for new customers.

Customer Education: Your team needs to clarify what kind of financing options you offer, and how it will affect their payment journey. Financing can add hurdles and time for the sale, giving more chances for the prospect to drop off.

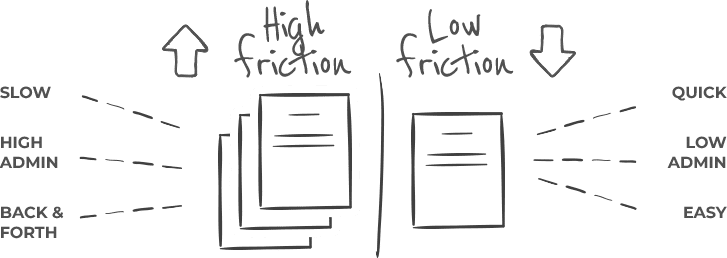

Administrative Burden: An application needs to be created and completed, taking time for both you and the prospect (no one likes to do paperwork in the evening or on the weekend!) Further, you can hit delays and chase paperwork back and forth with either the prospect or financing provider.

How to Reduce the Friction of Financing

Done correctly, contractor customer financing should be a boon to your sales strategy. The question is, how can you implement frictionless appliance financing?

By making the application process simple, completable by the prospect without your team’s input, and able to receive a decision within a couple of minutes, you can turn financing appliances into a streamlined option that drives sales. Easy, right?

These may all seem like things that are out of your control, but the good news is there is sales software that will do this for you. By offering finance options through a self-service portal, prospects can fill in an application form instantly and receive a decision within minutes. No paperwork needs to pass through your hands, the customer is happy as they’ve split their bill, and you made a sale you otherwise could have lost. It’s a win-win situation.

Simplify and Digitize the Financing Application

Much like your sales process, digital options streamline the application and approval journey. In comparison, paper-based applications can cost your business in time and printing fees. Further, this solution ensures documents don’t get lost, makes it easier to collect signatures, and facilitates passing information onto financial providers. No one wants a lengthy sales process!

Offer Quick Credit Decisions

Depending on your in-house team, or financial partner, your team can stand apart from competitors by incorporating soft credit checks into your regular sales process. Your sellers can obtain verbal or written consent to pull your prospective customer’s credit. (Note, confirmations over the phone must be recorded). Seamlessly incorporating financing and credit checks into your sales conversations ensures prospects can get approved sooner.

Offer Incentives

Prospective customers want to feel cared for and catered to. You may be able to provide reduced service fees and interest rates based on your financing partner, and financial system. Offering incentives ensures more customers can get the exact services they want, without having to compromise.

Communicate All Financing Terms Transparently

Not everyone is an expert in finances. It’s crucial to break down your offerings into the simplest terms. Further, these conversations are great opportunities to educate customers about all the benefits of financing. Your prospects will remember and appreciate your team’s excellent customer service.

With offering financing to customers covered, let’s move onto Chapter 5, where we’ll cover how to measure success through sales reporting.

Question

Do you wish you could offer financing to customers more regularly?

Of course – it’s a win-win! Your biggest challenge to offering more financing is the admin burden and the back-and-forth of completing an application. Eliminate those and there’s no reason that your customers can’t finance jobs more regularly – and with less friction! If you’d like to hear about a new way that trades businesses can offer appliance financing seamlessly, register your interest here.

Okay! While financing is a great way to attract and win customers, it doesn’t make sense for all types of trades business. If you’re curious to learn more about the impact of appliances financing in the trades industry check out our video with Vendigo.